LOGIN

LOGIN

- Dollar General’s results where consistent and “more consistency” has been management’s goal for over a year. They delivered that this year and the 2026 outlook was for continuation of that.

- Like in the off-price / treasure-hunt retail industry (our note here ), Olli’s is benefitting from greater disruption in adjacent industries. For Ollie’s, this is the conventional grocery and snacks industries.

- Neither company suggested any near-term favorable lift in demand from this tax season’s increased refunds. Both were hit by February’s adverse weather.

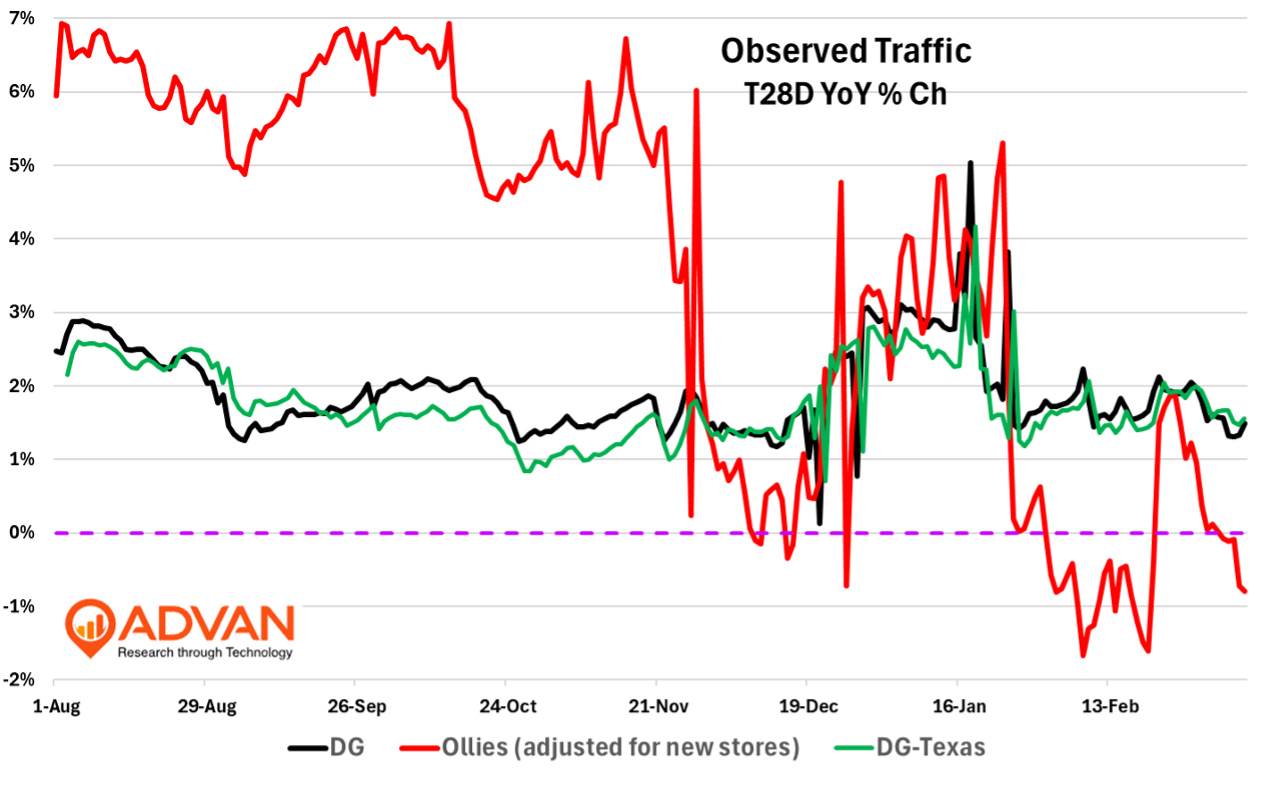

For FQ4, Dollar General (DG) reported increases of +4.3% / +2.6% / +1.7% for comp-sales / comp-transactions / +1.7% comp-ticket. **Observed traffic and average ticket **increased +2.2%* / 2.5% respectively. As shown in the traffic chart, to a degree, the quarter-to-date traffic was impacted by the winter storms (Ollie’s more so). However, DG’s trend in Texas (and Florida for that matter) still looks similar to the nationwide trend, i.e. softer in February. Moreover, softness also demonstrates that there has been little lift from this year’s higher tax refunds (as many market commentators had hoped / hypothesized). DG’s discretionary categories like seasonal and home outperformed (as they have all year) and that boosted sales, ticket, and gross margin rate. Congrats to its merchants for getting the right mix and value into the stores. A decline in units-per-transaction (UPT) suggests that traffic is somewhat bolstered by a paycheck cycle effect. Consistent with management’s comments, there has been little change in DG’s customer mix since Q4’2023**, i.e. its customer gains are evenly spread across customer segments. Guidance for FQ1 comps was “the low 2s”, i.e. conservative (especially in light of the recent surge in oil prices), but in line with the observed February traffic and ticket trend. (Easter aligns better this year April 5th vs. April 20th in ’25).

On its new 3P delivery initiative, DG’s CEO Todd Vasos said, “We have significantly expanded the reach of our delivery options available to customers and are now delivering customers through approximately 18,000 stores and with our own myDG delivery offering, as well as through third-party partners, DoorDash and Uber Eats. Collectively, these delivery options have significantly enhanced the convenience proposition for our customers with more than 80% of the orders delivered in 1 hour or less while also extending our value offering to a wide range of new customers who were previously underserved by delivery options in their community. As we continue to see larger basket sizes than an average in-store transaction and very strong repeat visit rates, our rapidly growing delivery platforms are becoming a more meaningful sales driver. In fact, we estimate delivery sales contributed approximately 80 basis points to our comp sales growth of 4.3% in Q4.” (Advan isn’t sure how exactly this is impacting observed traffic and transactions. Advan likely captures a portion of the traffic, but transactions are likely recorded elsewhere.) On DG’s retail media network, which is related to DG’s digital surface and 3P deliver***, Vasos, “In 2025, as partners continue seeking access to our unique customer base, we delivered approximately $170 million in retail media network volume, which is highly accretive to gross margin.”

Ollie’s Bargain Outlook (OLLI) reported a comp-sales increase of +3.6% and observed traffic and average ticket (adjusted for new stores) increased +2.3% and +1.3%, respectively. Signups were strong with new memberships in our Ollie’s Army loyalty program increasing by +23% and the total customer file increasing by 12%+. In terms of new markets, OLLI entered Minnesota in the quarter (35 states now) and plans to enter New Mexico in ’26; longer-term, management continues to target more than 1,300 stores (658 currently). On the disruptive weather, CFO Rob Helm said, “The end of January caused a significant number of store closures and disruptions to the business. Given our store geography, we were particularly hard hit by the weather.”

On merchandise availability, CEO Eric van der Valk, said, “Deal flow for us, it’s off the charts. With the consolidation of retail that’s taking place, definitely outsized consolidation in retail over the past year. We are seeing deal flow in just about every category that’s off the charts. And again, I mentioned consumables, but that’s definitely been a strong pipeline for us in consumables. So we’re extreme value retailer.” Per the strong pipeline in consumables, one of Advan’s big themes is the significant share transfer of pantry-load / center-store categories from conventional grocers to Amazon, Walmart, and the club channel. As such, we are left wondering if Ollie’s is benefitting from conventional grocers cancelling orders for center-store items and then that inventory (on the producers’ / wholesalers’ balance sheet and in their warehouses) finds its way into Ollie’s stores. (Nearly all national CPG food brands are experiencing negative channel mix. Why isn’t Grocery Outlet also benefitting from this?)

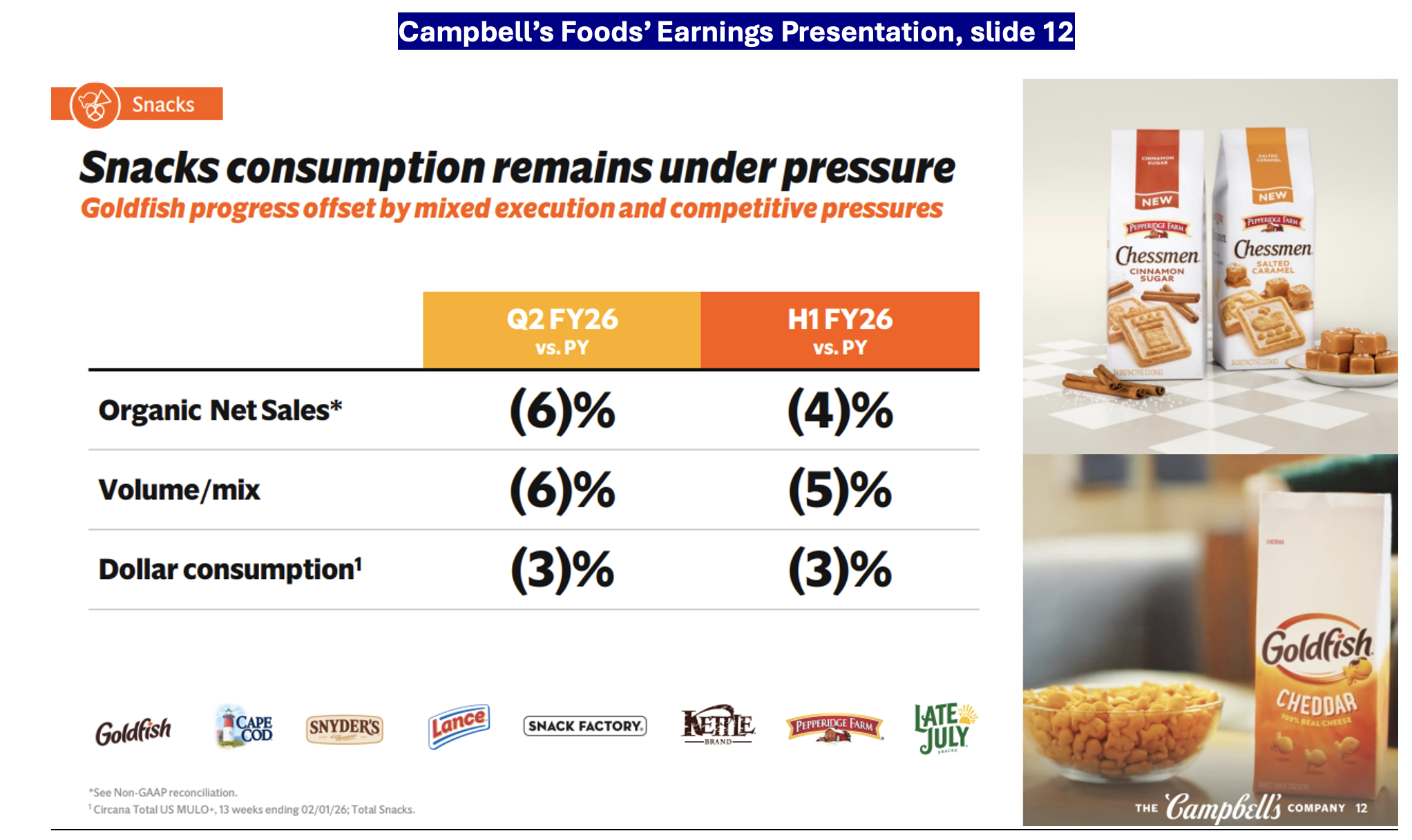

This week brought our theme to light again with Campbell’s reporting disappointing results; Campbell’s earnings for its fiscal year are now expected to decline -25%, a reduction from its prior outlook of -15%, with the guidance reduction due to weaker volumes and a weaker channel mix. Another driver of strong availability in consumables for OLLI may be that Frito-Lay recently won a significant increase in shelf distribution; Pepsi’s CEO Ramon Laguarta said on its Q4 call, “Just to give you a number, the average space gain for Frito-Lay in the new resets of both the main aisle and the perimeter will be double digit. So we’ll be growing double-digit space in Frito-Lay from the March, April time frame when most of our partners start changing their layout. So this is a good return for us and a great return for the category as well. And this category needs to grow. It’s very relevant for our partners, it’s relevant for us.” That’s a lot of disruption in the snacking shelf space and it doesn’t reflect more shelf space for the category, it means less shelf space for competitors, like Campbell’s. As such, that leads to less sell-in by Campbell’s into the channel; moreover, in the short-term it also means more liquidated and cancelled orders – product that OLLI likely bought up on the cheap. On its chip business for the quarter, Campbell’s said, “Turning to Salty Snacks, the sequential progress within Pretzels was offset by competitive headwinds in Chips.” Overall, this is why the volume / mix component, shown in the slide below at -6%, is worse than the dollar consumption figure of -3%.

See our last write-up on industry trends here and here , and the last results from the dollar stores.

‘* Others had DG’s traffic per location at +6.5% and +200bps stronger QoQ. Reported comp-transactions were only +10bps QoQ (Advan was +22bps QoQ) and the 200bps vs. 10bps delta may partially explain why the stock was weak on the results. “** This is a CQ4’25 vs. CQ4’23 comparison. Advan + Spatial.ai segments visitors into 80 psychographic cohorts for any given period of time. Looking at changes in the cohorts between time periods allows one to see which cohorts are growing / holding flat / declining. “*** DG makes a lower contribution margin / $-profit on the 3P delivery order, but that’s largely made up with brand spend on DG’s media network.