LOGIN

LOGIN

- Grocery Outlet reported another quarter of below plan sales, that along with a soft 2026 YTD trend and a review of new store performance (classes from ’22 – ’25) has lead management and the Board to conclude that the most favorable outcome is to close 36 locations (especially in Maryland and Pennsylvania), as well as to evaluate selling its recently acquired United Grocery Outlet chain.

- Overall comp-sales have been pressured by fewer items in the basket (UPT) as shoppers are not finding the WOW! values that they expect.

During this “epic period of value,” that Grocery Outlet (GO) has struggled to drive comp-sales and is now shuttering locations (-7%) is “provocative” to say the least. For context, Aldi grew comp-sales by around +4% in ’25 and Trader Joe’s by around +5%. By contrast, GO was only +0.5% for ’25 and -0.8% for Q4’25. That underperformance is also reflected in Outlet changing management during the year; new CEO Jason Potter was placed in February. Given that it’s been a year since the appointment, clearly, he gave the new classes of stores a year to shape up. Some didn’t and he’s focusing on those in the East. As a reminder, GO acquired Tennessee-based United Grocery Outlet (40 locations). It’s unclear if some of those are part of the planned closures (36). Since 2023, GO has added 12 new locations in Maryland and 11 in Pennsylvania. In 2025, the Maryland stores produced 70% of the nationwide traffic average, and Pennsylvania’s locations, only averaged 60%. The chart below shows new store productivity (in traffic) by class of opening. As shown, the new store productivity (NSP) trend has deteriorated each of the past four years.

On the earnings call, Potter said the following:

“As we discussed in our last earnings call, beginning in late September, comp performance began to deteriorate. We shared that some of this was a direct result of decisions we made on marketing that were net negative and we responded by recalibrating our marketing mix and doubling down on in-store execution. With new leaders across store ops, merchandising and supply chain, we began accelerating our store refresh program based on encouraging early results. Following our Q3 call, November comps were weak. – driven in part by the timing of EBT distributions that negatively impacted our SNAP business and affordability pressure on our core customer increased more than we’d expected. Despite fishing Q4 with positive traffic, basket pressure intensified, resulting in a negative comp for Q4. Comp sales continued to decelerate in January, driven by declining units per transactions and slowing traffic growth. At that point, we took a hard look at the business from end to end, buying and supply chain, pricing and promotions, the customer experience and our store network… [C]ustomer survey and third-party research showed that while our base pricing was competitive, our leadership position on value perception had eroded. While we made progress by addressing KPIs, we needed to address value more holistically. Third, our push to improve in-stocks and add assortment to ensure the availability of everyday items squeezed our supply chain impacting our ability to deliver high-quality opportunistic product that drives value in this business. Shoppers came in looking for the value and the treasure hunt experience they expect from Grocery Outlet but left a few items per trip because we didn’t deliver the weight of WOW!”

– GO is a treasure hunt shop. Longer times in the store lead to more items in the basket (UPT), and that to increased frequency. The Pennsylvania stores, which should be benefiting from a favorable maturation curve, experienced stagnant dwell times, a decrease in frequency and visitors, and a slight increase in visits (+4%). Company-wide, the average transaction size declined -1.7% due to fewer UPT. And for Q1, company-wide comp-sales are expected to decline -2%. WOW! (or the lack there-of). Moreover, that outlook comes with material increase in the company’s promotional investment (roughly +$10 per quarter, or 85bps to net-sales.)

On the store closures, Potter said the following:

“Following a rigorous analysis of the fleet, we identified 36 stores in the network that we concluded did not have a viable path to sustained profitability regardless of the operational support we could provide. We’ve made the difficult decision to close 36 locations, 24 of which are located in the East, representing roughly 30% of that region’s fleet. We are not fully exiting any state, and we believe we have a meaningful opportunity to grow in the East over the long term. However, it’s clear now that we expanded too quickly, and these closures are a direct correction… These closures do not change our long-term view that ample white space remains ahead of us. And we continue to plan to open another 30 to 33 net new stores in 2026, but they do reflect a more disciplined approach. Going forward, we plan to expand with a more clustered model to improve supply chain efficiency and marketing leverage. We’re also adjusting how we go to market. We’re piloting new approaches to store openings to strengthen returns on capital. For example, as we launch our stores in Virginia in ‘26, these locations will start as company run with the intent of bringing them up to profitability before handing them over to independent operators. Once proven, we believe this approach could be applied in more markets as we continue to grow this business…”

On new stores beyond 2027 and the process of selecting locations, Potter said, “Our process over the last year on the network and growing is very much focused on sustainable growth and returns on invested capital. And key ingredients to that include site selection quality making sure sales productivity potential is there. Those things, I think, there’s a lot of real estate in the 36 that’s very challenged. We’re underwriting stores now, locations that have more potential. We spent time on lowering our CapEx costs the conversations we’ve had over the last couple of quarters include clustering, waiting to core markets, leveraging marketing, brand strength, supply chain and obviously, the operators are key… So clearly, we – growth is important, but we want to make sure that we’re improving the strength of the company as we do that.” On in the stores in the East, Potter, “We’ve modulated already the kind of mix of stores in core markets versus new, and we’ve done that over the last couple of quarters, which reflects some of the returns that we’ve indicated. In the East, in particular, the 51 stores that we have remain are all four-wall profitable, and they were comping over 3% in the last quarter. We think that the DC we just opened in the East… will greatly support the improved product availability that we need for those stores. And the work will continue there, but we’re probably going to go in a more measured pace in a place like the East than for sure what’s happened over the last 5 years.”

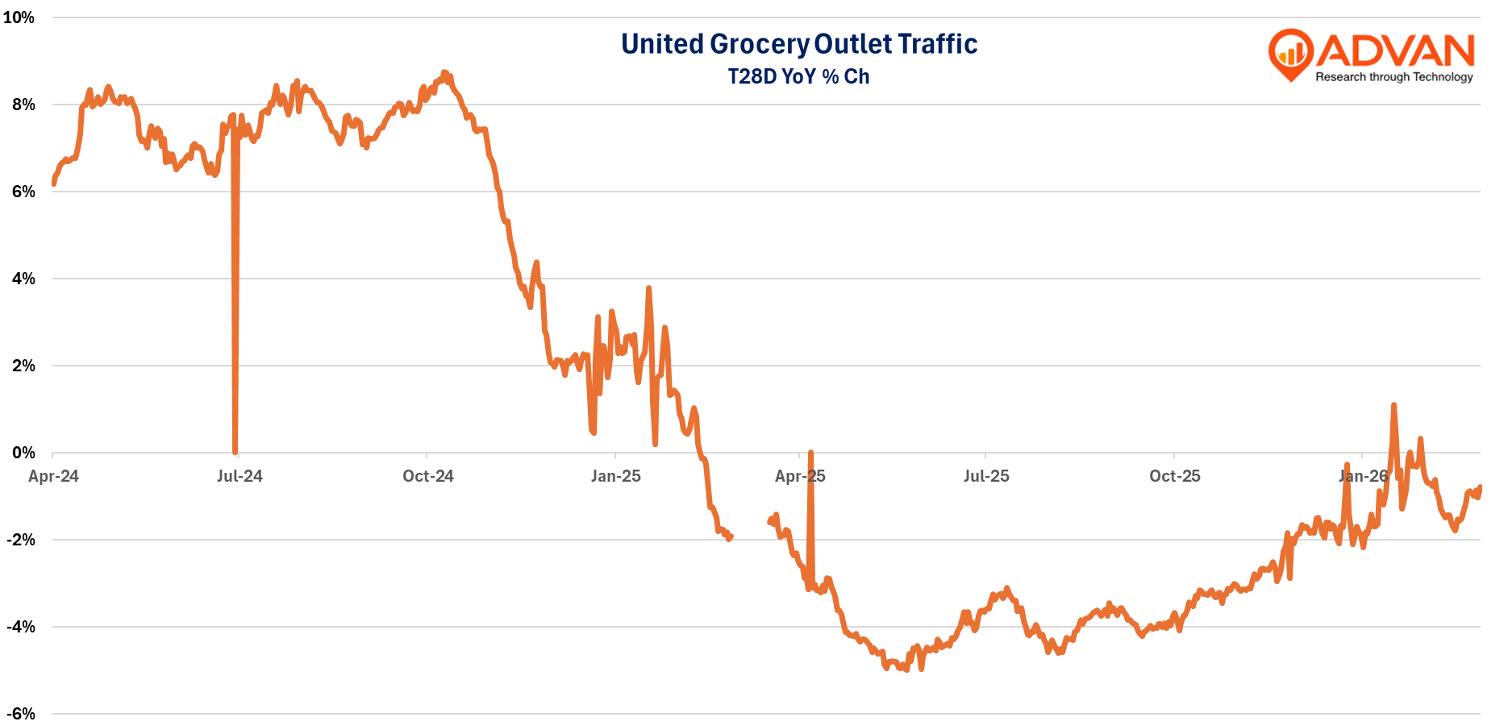

“On United Grocery Outlet, Potter said, “A strategic review of UGO. Finally, we’re scrutinizing every aspect of the business to remove distractions and improve shareholder value. To that end, we’ve made the decision to implement a strategic review of UGO. In an effort to focus on what’s important to returning this business to sustainable growth, we are reevaluating the organizational impact that would be required from a full integration of that business relative to the anticipated benefit.” – As shown in the chart below, traffic to the chain has been deeply negative during 2025.

A “strategic review” implies that it could be sold. Potter shared, “We have confidence in the business, the team there, the market, it continues to be profitable and stable. But given our priorities and the trend in the core business, we want to make sure we’re evaluating our options.”

See our last write-up on industry trends here , here , and here .