Last week, we wrote that we expected the pace of holiday foot traffic to accelerate going into Christmas day, and as shown below, that has happened; however, Advan’s transaction data shows that store spending has not, save department stores and off-price. The only segments where we observe average transaction size increasing are off-price, Dick’s Sporting Goods, and Apple. By contrast, Best Buy’s average ticket shows a lot of compression. We offer three possible explanations for the shallower store spending trend:

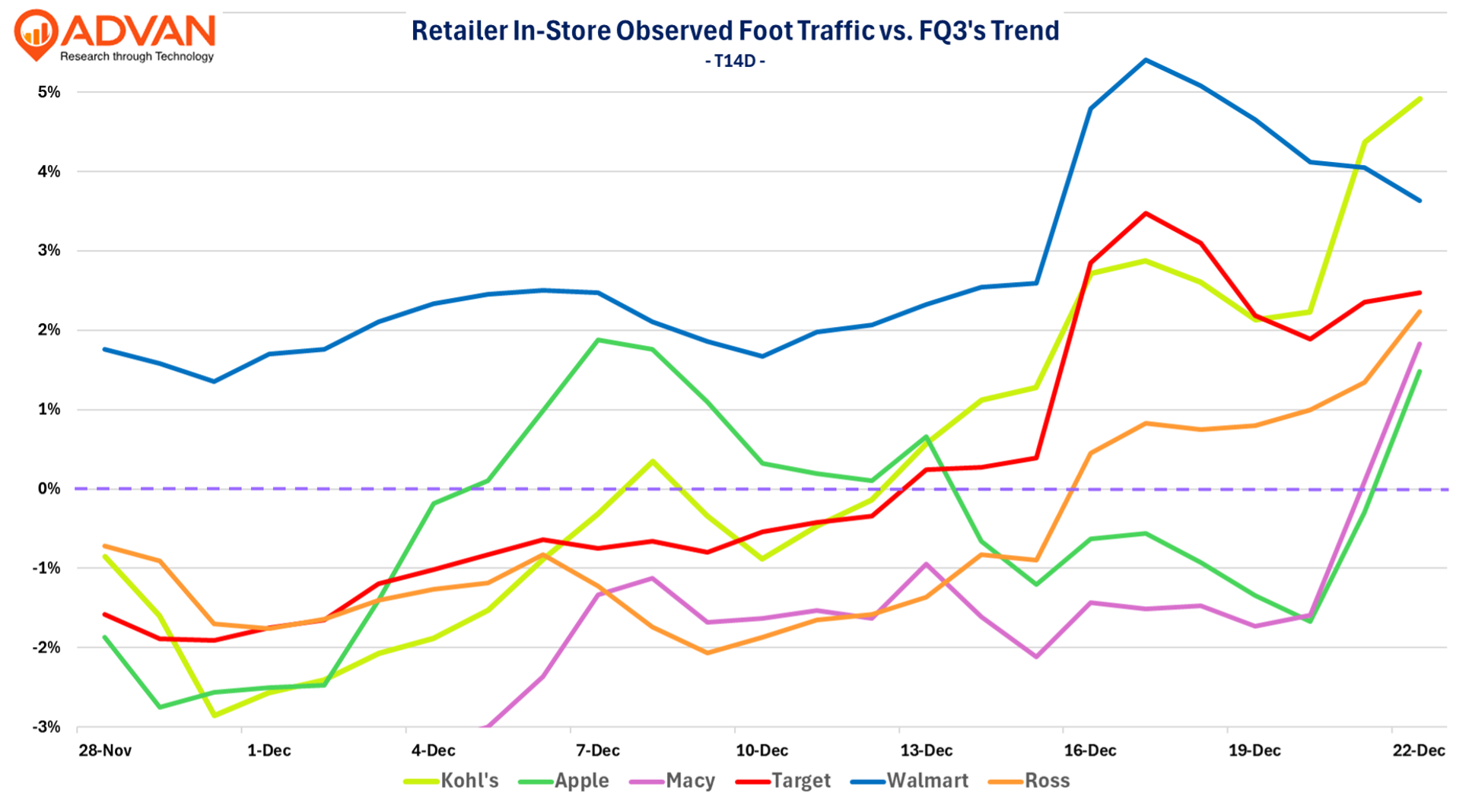

As shown in the chart below, the momentum in traffic has picked up across most brands, with Kohl’s and Ross Dress for Less showing the most dynamic improvements in performance. The chart shows the FQ4 trend relative to FQ3’s rate; on an absolute basis, Walmart observed store traffic (per location) has the most “festive” performance at +3.5%. Complementing that level of growth will be Marketplace, store delivery, and curbside.

In terms of observed spend, Five Below and Dick’s continue to have a gangbuster season. We’ve also read a lot of enthusiasm for Macy’s in the trade press; Macy’s pace of observed spend is exceeding Dillard’s, which suggests that they may out-comp them for the quarter given the high weight of December.