LOGIN

LOGIN

- As the re-Tarjay-fication of Target is just underway, top-line results for FQ4 were expected to be soft, and they were. The sales mix was also little changed. However, profit margins were favorable.

- The January trends improved despite the adverse weather at the end of the month. Shopping increased +2% for the month and visit frequency has stabilized. Both measures suggest early success with Target’s re-merchandising. Management noted that comps in Feb > Jan > Dec > Nov – just as observed traffic shows.

Target reported a -2.5% comp-sales decrease for FQ4; the -2.5% can be deconstructed into -3.9% from its in-store business, partially offset by a +1.9% in all other businesses. The -3.9% can be deconstructed into +0.4% from average ticket, offset by a -4.3% decline in traffic, both figures were very close to observed transactions (-3.9%) and spend. (New stores also added +1.0% to total sales growth.) Category-wise, apparel & accessories and home furnishing & décor were the weakest and those categories are where the Tarjay needs to get working. In January, the frequency of visits flattened out, and shopping increased +2%. (We define “shopping” as the total time spent in Target stores.) These two indicators suggest that both the shopping experience and the appeal of the merchandise are rising. (Improving the store experience is a central focus of CEO Michael Fiddelke – in stocks, remodels, and increasing the service levels and in-stocks, etc.) February’s observed trends were also a touch stronger MoM.

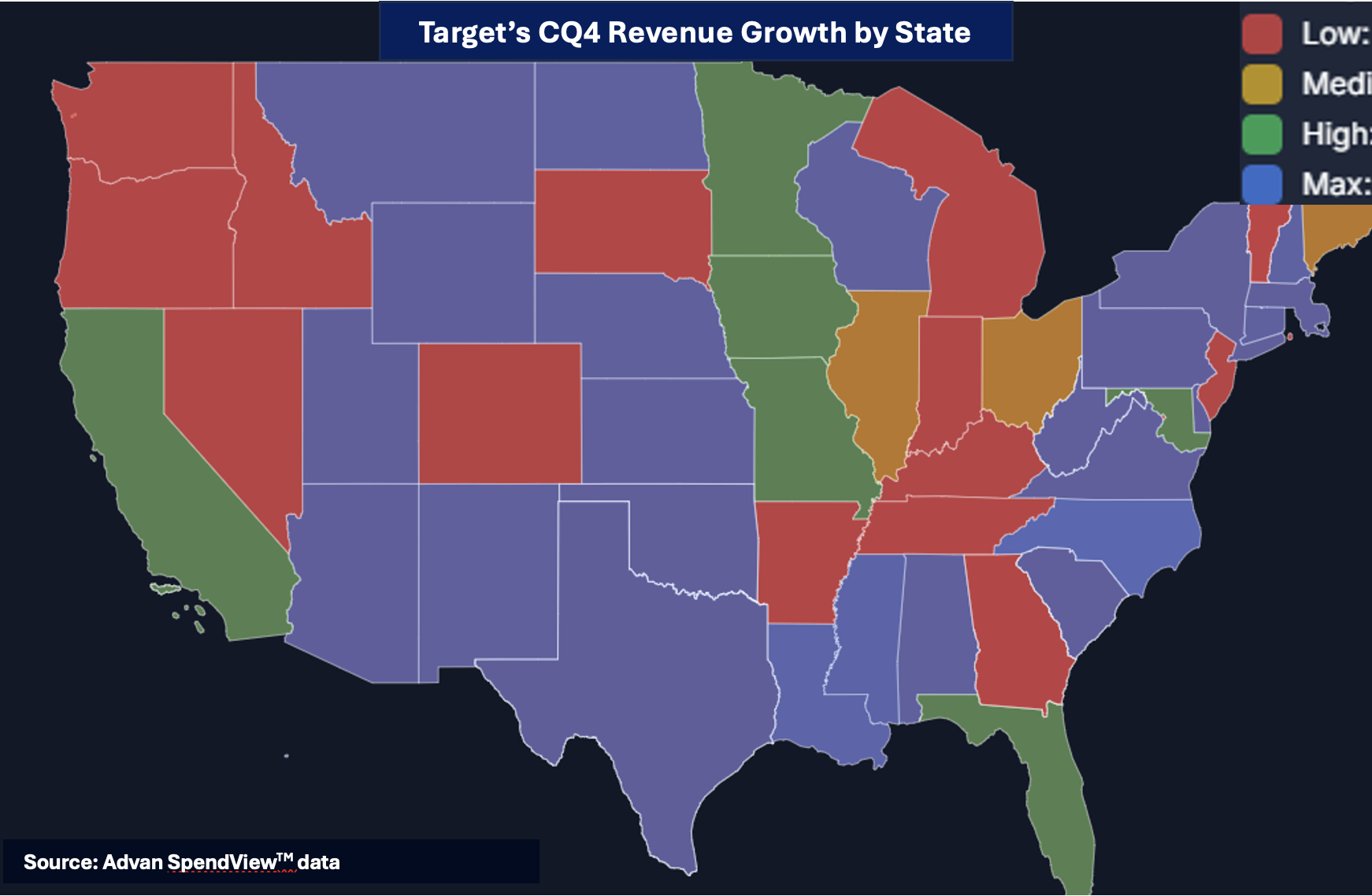

Regionally, Target experienced the most robust growth in the South and East Coast. The Northwest and Mid-Central regions were the softest, as shown in the figure below.

On how / where Fiddelke thinks Target can grow, he said, “The lane we’re uniquely suited to own and win in retail. That lane begins with our purpose of helping all families discover the joy of everyday life. And we’ll bring that purpose to life by being the most delightful experience in retail. Now those aren’t just words. Delight is a critical filter for decisions and informs our actions going forward. It encompasses what we consider foundational to a great shopping experience, convenience speed, price, yet consumers consistently say they want and expect more, especially from Target. So Delight is our standard. That means getting the basics right, sharp pricing, strong in-stocks, wicked fast, same-day delivery. Yet our bar is higher. We want to spark an emotional connection. So shopping isn’t a chore, it’s a joy… [On] merchandising authority is about curation and playing to our strengths. Target is not an everything store. That’s not what guests want from us. They want a strong trend-forward assortment that they can trust to deliver quality and value. And that’s exactly what we do at Target when were at our best. So we’re making choices. In assortment, we’re doubling down where we are strongest and where guests tell us are right to win and grow is highest…”

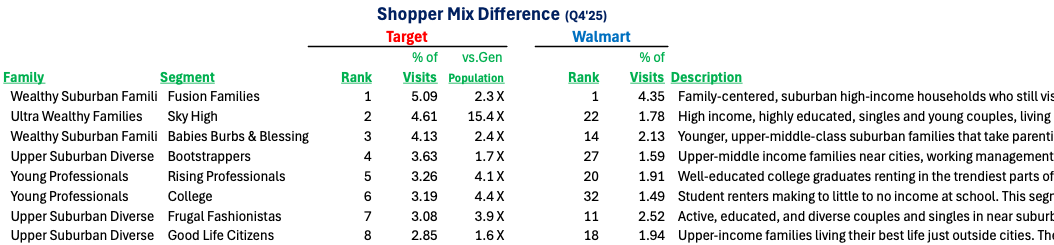

By Fiddelke choosing the word “lane” and that means they do not intend to be a retailer to all shopper types and that they will press to get more of their share from the types that do shop Target. What are those types vs. Walmart? The table below of shopper segmentation* between the two retailers. The Fusion Family segment (median household income of $110K) is the #1 segment (out of 80) for both retailers. By contrast, the Sky High segment (HHI $170K) is ranked #2, but #22 for Walmart. Moreover, its contribution to Target’s visitors is 15.4X the general population’s percentage. This is a segment that Target wants to win big-time with. Same said for the two Young Professionals segments shown and Frugal Fashionistas (ranked #7). Sky High’s high 15.4X ratio demonstrates that Target can strongly increase its penetration in any given segment, if they can deliver what Fiddelke and Target stives to do.

“* Advan + Spatial.ai segments visitors into 80 psychographic cohorts for any given period of time. Looking at changes in the cohorts between time periods allows one to see which cohorts are growing / holding flat / declining. See our last write-up on industry trends here and the last results from Target.