- Apple should report revenue acceleration for its Americas segment, powered by the iPhone.

- Equipment expense for the wireless operators should be much higher YoY (fueling the strong iPhone sales).

- Wireless gross adds should be up YoY, net adds, roughly even YoY, implying worse churn YoY.

- Cable should pick up the majority of net adds; T-Mobile’s exceptionalism has passed.

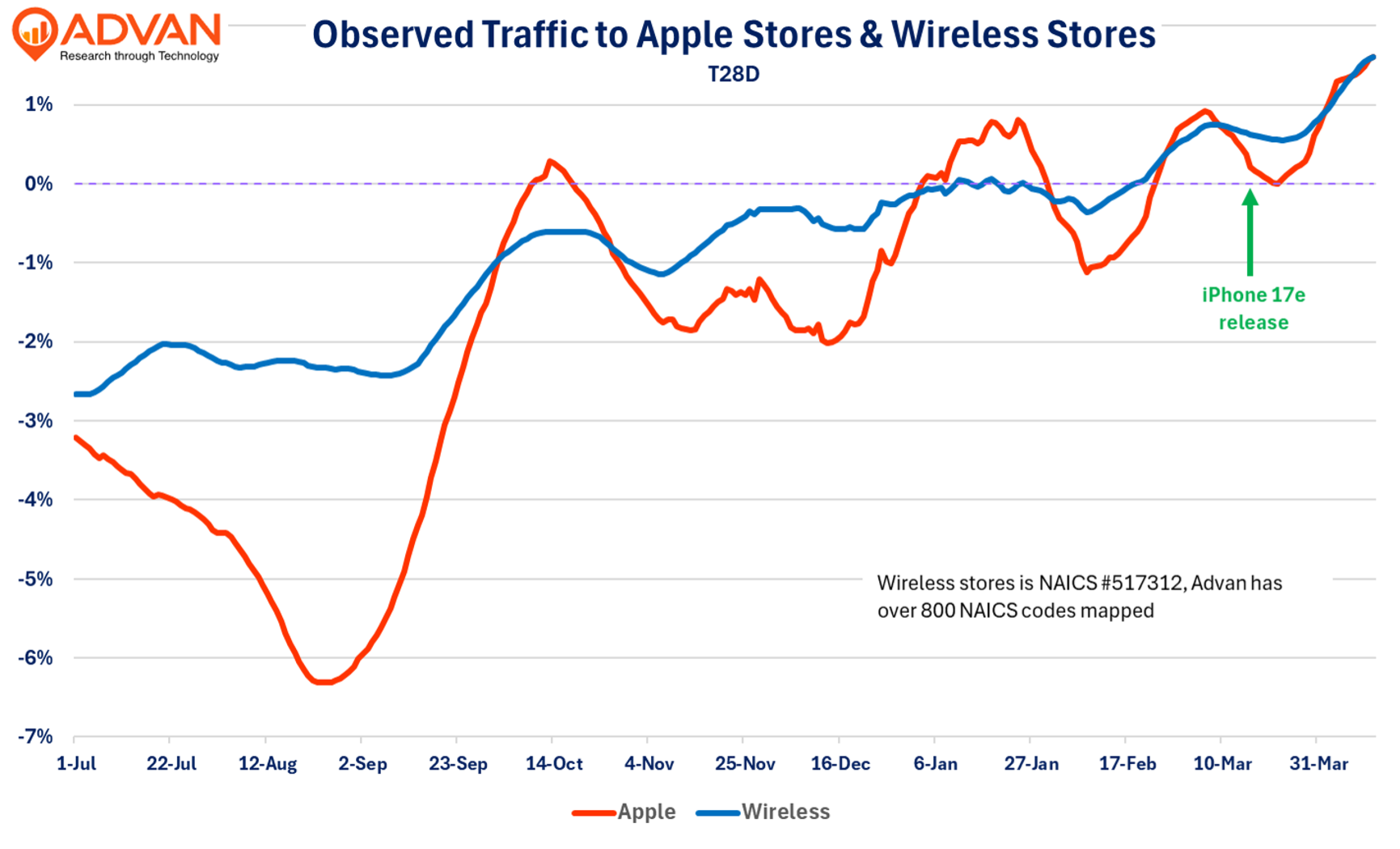

Advan’s data was quite foretelling to the Q4 results for the wireless industry and Apple, as such, we looked again at what the data suggests for Q1 results. The visitation trend at Apple’s stores continues to be robust, indicating strong sales results in the US for CQ1. Recall that Apple reported +11% revenue growth in its Americas region in CQ4, with sales growth held back by short supply. Supply should be better for Q1, allowing for growth above Q4’s rate in light of the stronger observed visitation trend. Additionally, it appears the iPhone 17e received a strong reception. Q4 results from the wireless industry (all in terms of postpaid phone) were marked by high handset expense (a plus to Apple’s revenue, a negative to the wireless industry’s profits), increased switching / churn, higher gross adds, and modest subscriber growth overall. Given that observed traffic to wireless stores remains elevated, Q1’s results should be a repeat of Q4’s.

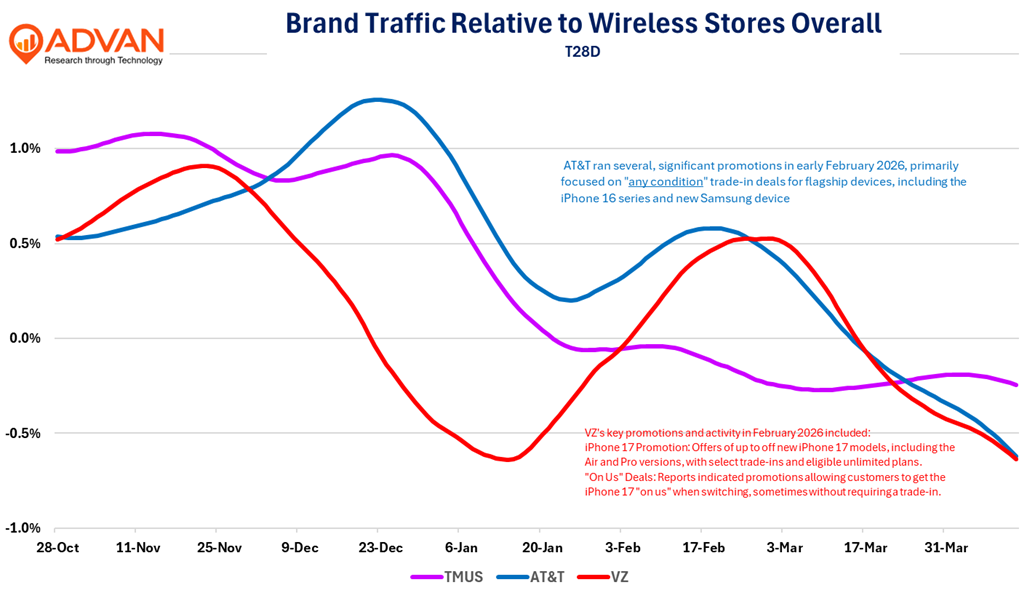

The chart above looks at observed activity vs. the overall NAICS code #517312, and it suggests that T-Mobile will be lighter in gross and net adds. (We do not have the ability to know why an individual entered a brand’s store, whether it’s to become a new subscriber, to churn, to add broadband, to pay a bill, etc.) Verizon and its new CEO are on the attack, and we expect another stronger YoY quarter of gross and net adds. We judge that because Verizon didn’t step up the promotion in March. (For Verizon, its most important guidance target is >750K postpaid phone net adds for the year.) Our read on AT&T is similar. T-Mobile is offering a free entry-level iPhone 17e (worth $600, no trade-in required) to new customers and Verizon matched the offer. We don’t, yet, understand why Verizon and AT&T didn’t benefit from the iPhone 17e release, whereas in March, T-Mobile’s trend outperformed.

We will be very interested to see if cable had a stronger result given the trajectory of observed visits for the Big-3 vs. the industry on a QoQ basis. We’ve seen estimates of stronger net adds for Comcast and Charter than T-Mobile, which would have been unthinkable a year ago. However, this “call” on T-Mobile net adds is a bit “whimsical” as T-Mobile will no longer disclose subscriber-level metrics (you want to guess why?)