Key Points:

· Grocery Outlet reported another weak financialquarter, but the underlying comp-traffic trend is improving (more promotions +better execution). Fewer items per basket continues to be a material drag. Thehigh number of store closures is creating noise in the data and with the KPIs.

· April retail sales were strong, as previewed;however, observed traffic (per Advan)is showing

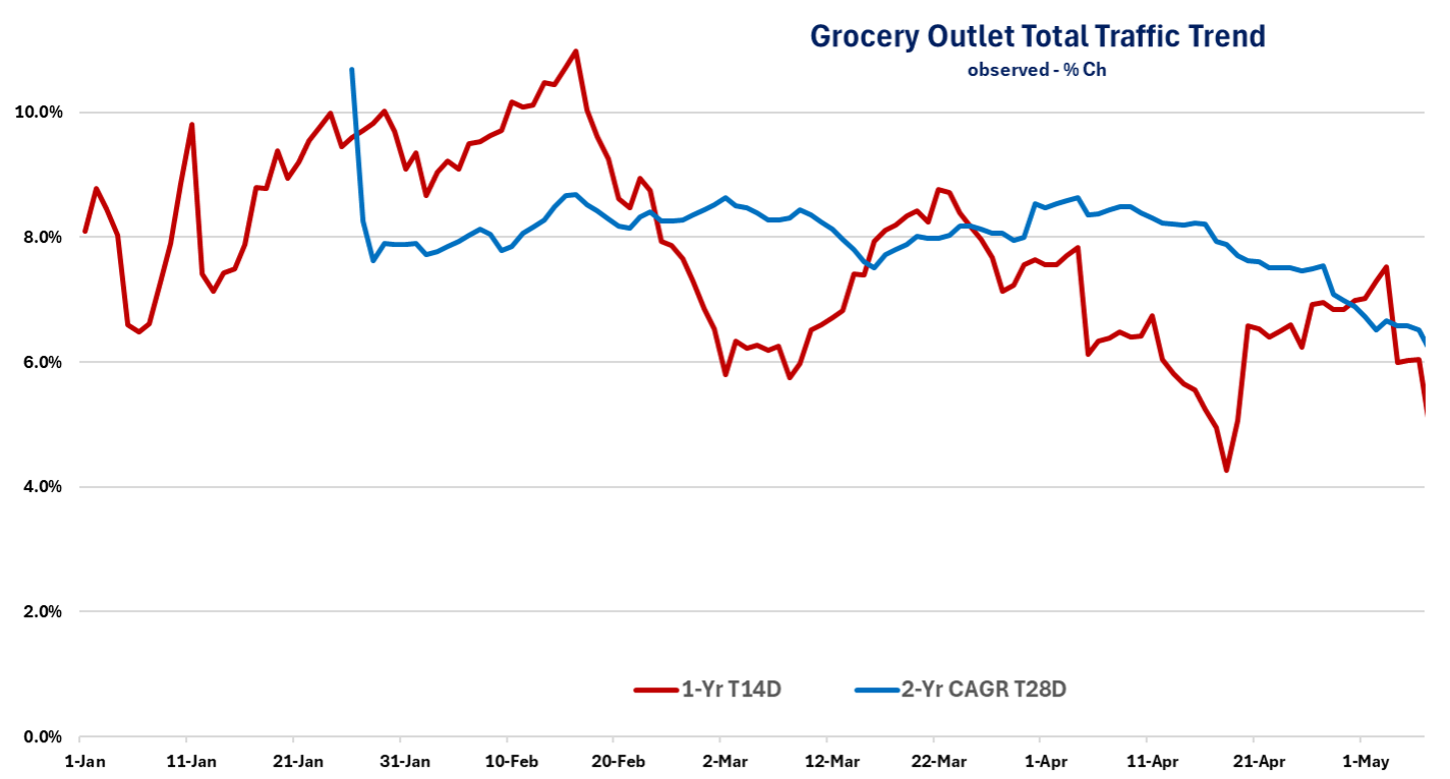

Grocery Outlet Q1results showed improvement in comp-transactions (+70bps QoQ, underlying) andstable observed frequency & dwell time,offset by a weaker comp-ticket (-3.1%), the negative impact ontop-line growth from store closures, and a large impairment charge for adecline in its market cap. Average ticket is now down -8% from its peak despite+5.6% inflation over the period; the decline is largely the result of feweritems in the basket (UPT). Guidance on Q2 comps was soft (-1.5% to -2%), butthat range leaves the 3-yr CAGR similar QoQ.

Management shared thatcomp sales improved month-to-month (Jan – Mar). That comp traffic was strongerin March isn’t a surprise given that they closed the “dog stores.” April observed traffic (per Advan) has slowedmeasurably due to the store closures; excluding that factor, traffic perlocation increased 5%. Management said that comp-traffic was +2-5% in March,and so, that suggests a further improvement on a comp-basis. However, May issofter. That is due to additional closures (9) and maybe the macro (more onthat in a minute).

CEO Jason Potter said,“Our job right now is to make Grocery Outlet a more compelling choice for thecustomer. In this environment, value matters more than ever. We must make thatvalue visible, consistent, exciting, and easy to shop. We executed on that inseveral ways during this last quarter. First and most importantly, we've mademeaningful strides to increase the mix of branded opportunistic products in ourstores. … Since the start of the year, we've increased our opportunistic mix bynearly 2 percentage points with meaningful improvement across inventory,shipments, variety and sales. We've made meaningful progress improving oursourcing, increasing product visibility, and helping operators furtherdifferentiate their stores. That works included upgrading systems andreporting, expanding supplier outreach, shortening delivery times, testingshort-dated offerings and engaging suppliers more directly at the leadership level.These efforts enabled us to move quickly in Q1 on excess inventory from severaltop-selling brands, delivering significant savings for customers while creatinghigh margin, high volume opportunities for us and our operators. Second, weinvested in reshaping value perception. As we work to improve the impact of ouropportunistic supply, the near-term synthetic promotional support we'reproviding is driving customers into our stores… We're sharpening our value messaging throughour extreme value campaign. This work is focused on making our valueproposition unmistakable, highlighting the significant savings customers canfind on branded products often at meaningful discounts to conventionalretailers and reinforcing the excitement of the treasure hunt experience thatdefines Grocery Outlet. To support this, we're driving awareness throughtargeted at home and digital campaigns that bring our deals and productdiscovery to life.”

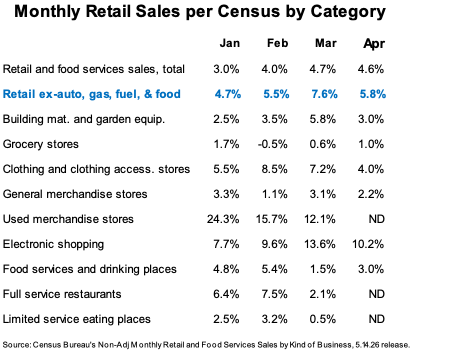

Turning to theconsumer, April retail sales, and some caution on May. April retail sales (asreported by the Census Bureau) were strong as previewed, but slightly below ourestimates. However, March was upwardly revised and we expect that same willhappen to the April numbers when the revisions are released in next month’srelease. The biggest negative surprise in April was the slowdown in clothingand clothing accessories stores (recall our theme that the apparel category isexperiencing a super-cycle fueled by the rapid update in GLP-1 drugs.) As such,we will be carefully reviewing the April PCE report on May 28th. Asshown, April was a stronger month for grocery.

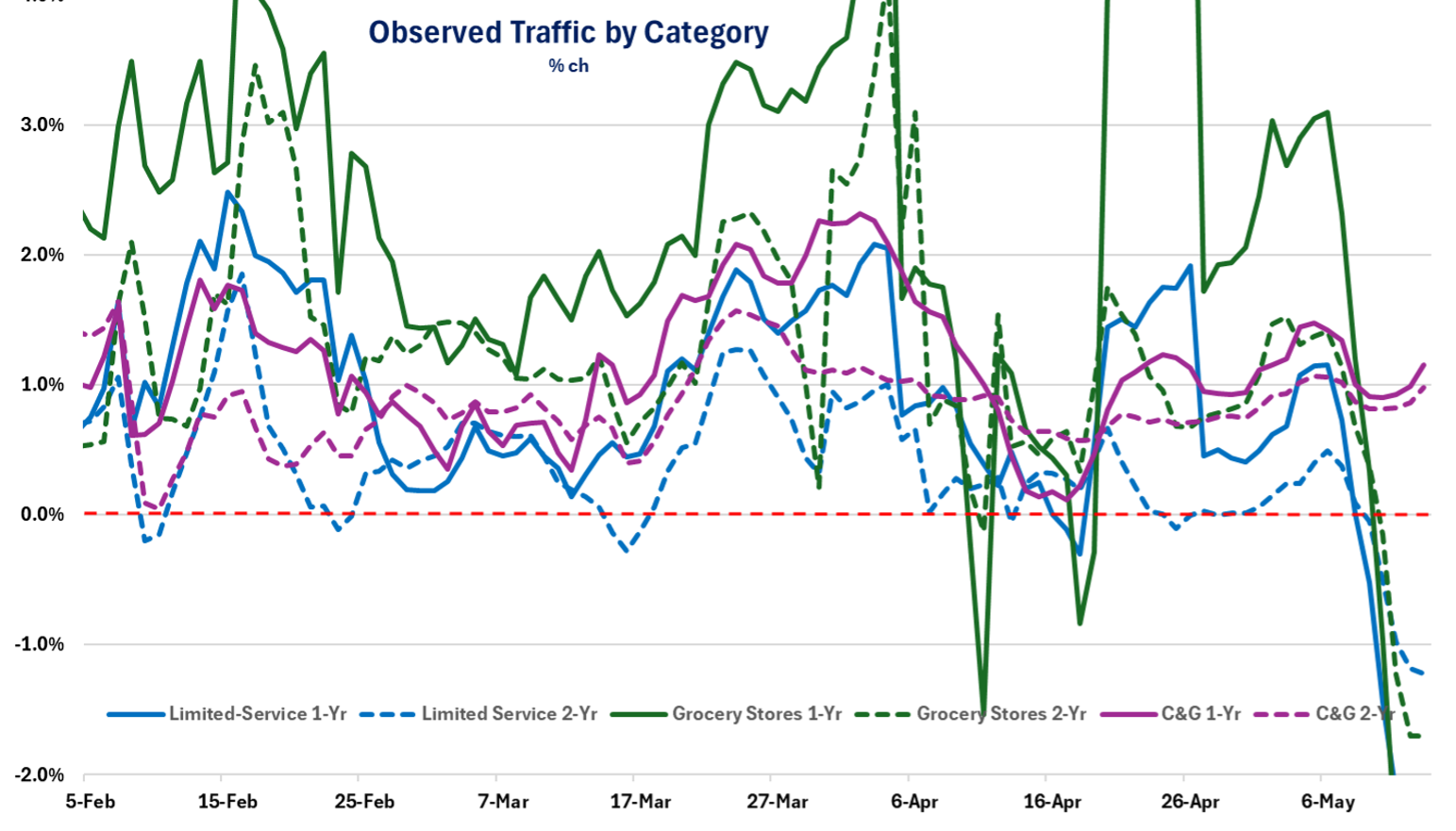

Interestingly, May’s observed traffic (per Advan) for grocerystores and limited-service restaurants has softened. By contrast, gas &convenience, dollar stores, McDonald’s*, Aldi, and Walmart have remainedresilient. The softness may be due to a set of consumers feeling fatigued dueto high prices at the pump. Earlier, less-affluent households could potentiallysustain the increased prices because they were believed to be temporary, butnow that we are 10 weeks in, the burden has become more lasting, and as aresult, households are making adjustments. This past week, General Mills andKraft-Heinz noted that trends have softened. That was also shown in the latestweek in scanner data. (Note the volatility in grocery stores during March andApril is due to the timing of Easter; that appears to be a factor forlimited-service as well.)

‘* We’ve read some sell-side reports citing weakertraffic and spend data for McDonald’s in April. Advan’s observed traffic andspend data show over +20bps of acceleration MoM, and so, we believe thesereports lack merit. Moreover, the note’s suggested degree of decelerationdoesn’t line up with management’s tone on the May 7th earnings call.