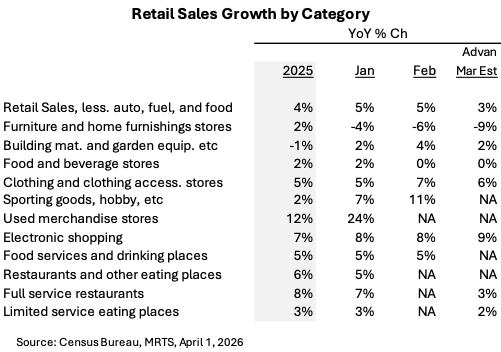

· Retail sales growth in January and February was very strongper Census’ report. Per Advan, March was softer due to adverse weather andconcerns / impacts over Iran / oil.

· Many of 2025’s notabletrends continue to dominate 2026 – including GLP’s impact on apparel, sportinggoods, grocery, and restaurants. Treasure hunt value (from Costco tosecondhand) is also strongly outperforming. In grocery, conventional grocersand conventional national packaged food brands continue to face challenges. Wesee little cause for relief to those challenges, especially if higher commoditycosts flow into the US food chain.

· Is March’s softer pacejust a bump, or is it the start of a trend? The 1H of April (after Easter) willtell.

The Census Bureau’s February monthly retail sales report, along with a positive revision for January, shows solid strength in consumer spending for the start of the year, as well as a continuation of heightened spend growth for two of 2025’s winners – apparel and secondhand. Apparel is in a “super-cycle” fueled by the uptake of GLP1s for weight loss, and secondhand is fueled by the vintage fashion rave and the K-shaped economy. (See our intro to 2026 here.)March’s activity stepped down from the strong Jan / Feb pace due to: adverse weather, the “CNN effect” of Iran / oil, the fall in equity markets, and growing consumer unease about employment and inflation. We see the weather impact in softer full-service restaurant visitation and an acceleration in fulfillment center activity (i.e. Amazon). Costco will report its March sales results in the coming week; Costco’s observed traffic was similar MoM, with any dampening from the weather being offset by strong visits to the fuel centers. That said, Costco’s traffic in California was similar MoM at +4.7%, and so, maybe its great treasure-hunt and deep value were similarly strong MoM. (Sam’straffic in California was +2.1% in March, slightly stronger than February’s +1.7%)

Delving into the retail categories of the report:

Our conclusions, the pace at discretionary retail during March is a step down from January / February’s very strong +5% pace. GLP1s are providing a lot of tailwind to apparel and sporting goods retail. Brands and retailers need to get themselves on the right side of this very meaningful consumer trend as the impacts in 2026 will be larger than last year. Lastly, secondhand’s outsized growth is a signal that vintage and value are in high fashion. Brands and retailers can also play to that, but only in an authentic manner. One example - see what Levi’s is doing; observed spend on the brand was very strong in February / March.

See our last write-up on industry trends here.