Key points:

- Advan’s data and the results and commentary by these four provide strong evidence that there has been no pullback by the consumer in response to higher gas prices or other macro concerns.

- Starbucks’ results demonstrate that Starbucks is “Back to Starbucks” with its strong top-line beat for CQ1, growing profits / margin rate, and increased guidance.

- Chili’s and Taco Bell “comp-ed the comp” (again) with positive comps on top of very high comparisons.

- Sysco’s US Foodservice division was (again) driven by outperformance of its non-national chain customers.

- Should you want to talk about any of this, send me an e-mail.

Well, Starbucks is “Back to Starbucks” with its strong top-line beat for CQ1, increasing profits / margin rate, and increased guidance (global comps for the year now to hit +5%+ from the prior +3%+). The new rewards program, menu innovation, showing the love the Green Apron crew, and investments / changes in the coffee house are all contributing. US comp-sales / -transactions / -ticket grew +7.1% / +4.3% / +2.7%, for a QoQ improvements of +310bps / +130bps / +170bps (vs. Advan observed figures* of +240bps / +110bps / +130 bps). Observed frequency of visit was flat YoY. One of CEO Brian Niccol’s primary strategies was to return Starbucks to being the third place in customers’ lives (see our prior stories here and here, and industry presentation). In terms of observed visits by daypart: 5am -10am grew 200bps faster than the average, 10am – 2pm, at the average, and after 2pm has opportunity (which management is working on in terms of menu innovation). As it relates to observed regional trends, California traffic was slightly behind the nationwide average, Florida was ahead, and when weather improved, New York was at the average. Overall, April is up from the pace in March and February, i.e., no evidence of a pullback due to higher gas prices or other macro concerns.

On the store remodeling program, Niccol said, “Customers are responding to a great coffeehouse experience. Coffeehouse uplifts are driving positive customer feedback and transaction trends, reinforcing the role of the coffeehouse experience in our return to growth. We're investing in that experience at scale with more than 300 uplifts now complete... We're accelerating this work over the next 2 quarters and expect to have more than 1,000 uplifts completed in our top 20 markets by fiscal year-end (ambitious to get that across 8,000-plus stores in very short order). Our return to growth has also sharpened how we manage our coffeehouse portfolio.” 33 net new locations were added in the quarter, to end at 16,944, (+80 more planned for the next two Qs) and additional measures were taken to densify the South and Southeast markets.

On the overall rising level of competition in the market (the topic of our presentation; e-mail me for it), Niccol said, “What I think is -- we're seeing is just the reality that more and more customers are interested in drink experiences, whether that's morning rituals or afternoon experiences. And I think you're also seeing customers or consumers, frankly, at all different age cohorts wanting to have a Third Place experience. And so look, it's almost, I think, a complement to the fact that our refresher business is being imitated in so many places… I believe the innovation that we're bringing to refreshers, the innovation that we're bringing to coffee, the innovation that we're bringing to espresso is going to continue to position us really well in culture. And it's also going to position us well to lead on kind of the growth side of the category that we're going to continue to see. So I think it's a great sign. It's a telling sign that we're actually responding to what customers want. And I think others are trying to imitate and I think we're in a great place with our scale and with our innovation and the pipeline that we've got coming really across how people want to experience drinks.”

Brinker

Brinker’s Chili’s again “comp-ed the comp” with a +4.0% comp (against a +31.6%) and the release quoted, Kevin Hochman, CEO of Brinker, "Guest demand remained strong in the quarter, recovering quickly after significant weather headwinds in January, driven by continuous improvements in food, service, and atmosphere, along with unmatched everyday value." Chili’s comp-transactions+mix / -ticket were -0.6% / +4.6% (for QoQ deltas of -480bps / +20bps). Advan’s observed figures were +0.3% / +3.8%. Observed traffic for Jan / Feb / Mar / Apr was -0.8% / +1.4% / +0.4% / +1.3%. Again, no evidence of a pullback due to higher gas prices or other macro concerns.On Chili’s compounding success, CEO Kevin Hochman said, “Hospitality, our differentiated customer service that drives memorable experiences to grow sales and traffic over time. While our competitors ramp up limited time offers, we spent the quarter investing time in operations, training and culinary resources into everyday capability that more closely correlates with long-term sustainable traffic growth. We believe doing fewer things bigger and better is a more sustainable way to build traffic and grow our business over time… [What’s next for driving FQ4’s comp]- we spent Q3 continuing to work on the fundamentals, preparing for our new chicken sandwich platform launch [April 14th] and bringing in new guests with relevant marketing to experience Chili's... From a food standpoint, our primary focus was chicken breading and cooking perfection, which involved retraining the teams on perfect execution of hand-breading our chicken crispier and chicken sandwich lineup, which will ensure those items are freshly cooked, hot, and crispy. A key differentiator of our chicken sandwich is that we hand-bread the chicken in restaurant. We believe a freshly breaded filet tastes better than chicken that has been breaded and fried by machines in a factory, frozen, shipped hundreds of miles, and then refried in a restaurant...” (Since the launch, the observed traffic trend has improved by +100bps.)Hochman, “A question we get asked a lot is with all the traffic growth you've had in the past few years, do you still have capacity for more? So let me start with the numbers. Our average traffic is now back to 2013 traffic levels, but that's still about 20% less weekly guests from our peak in 2000 to 2005. And our North-of-6 restaurants serve anywhere from 20% to 80% more guests than our current average restaurant traffic. So the first point is we know we have a lot more capacity in the buildings.” (“North-of-6" initiative refers to an internal benchmark for high-volume restaurants serving over 6,000 guests per week.)

Yum Brands

Taco Bell also comp-ed the comp with a +8% against a +9%, and +1 ppt stronger QoQ. (Yum doesn’t disclose traffic / ticket.) Advan’s observed traffic / ticket per location were 1.0% / +7.4%, +50bps / +240bps QoQ. Observed traffic per location for Jan / Feb / Mar / Apr was +3.0% / +0.6% / +0.3% / +3.5%. Again, no evidence of a pullback due to higher gas prices or other macro concerns.On Taco Bell’s future momentum, CEO Chris Turner said, “Why does Taco Bell continue to perform, it's really about delivering what consumers need in any environment. It's not just one thing, it's multiple things. That's grounded in structural advantage. The Mexican category is growing ahead of the overall restaurant space, and Taco Bell is a category of one in that space. We also have a business model there that allows us to deliver value while also ensuring high margins for our franchise partners… And of course, we deliver unbeatable value. The Luxe Value Menu that we revamped in Q1 is performing very well. 1/3 of all Taco Bell tickets have an item from the value menu there, and people are really building meals with a lot of variety using the value menu. So lots of strength, but we're just in the starting stages of the strategy that Sean laid out. So we're very excited about future continued momentum in Taco Bell.”

Sysco Foods

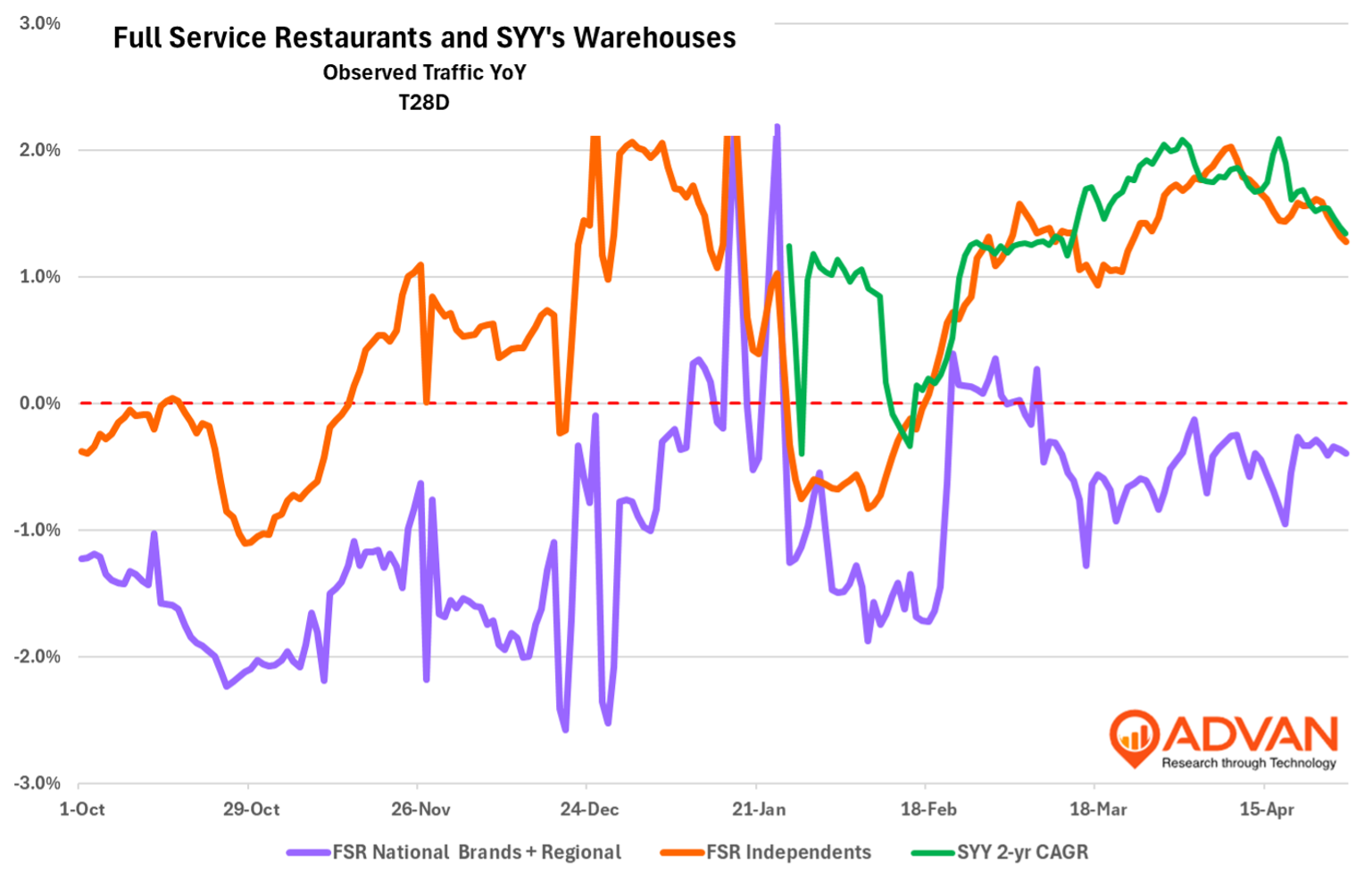

Sysco’s US Foodservice division reported volume of +2.3% (+150bps QoQ) with Local volume (non-national chain business) volumes increasing +3.3% (+210bps QoQ). Its Broadline volume (national chains) was described as soft, as it has been for some time. In the chart below, we show foot traffic to the nation’s full service restaurants in two indexes, one that is largely national + regional brands** (487K locations in total) and one that includes a large number of independent establishments (329K locations in total). As is evident, the locals index has outperformed the national index over the past seven months (and prior to that), which is what’s driving Sysco’s Local volume. The chart also shows that after a dip in US Foodservices warehouses activity in late January, a dip that aligns with traffic to FSR, activity has since rebounded, along with the indices.