Key Points:

- Nominal core consumer spending and retail sales were strong. Part of the top-line strength is in inflation, but even the core is stronger than Q1’s trend.

- Given the drop in gas prices, some of the lagging categories (for example, limited-service restaurants) should firm up for June’s reports.

- Should you want to talk about any of this, send me an e-mail.

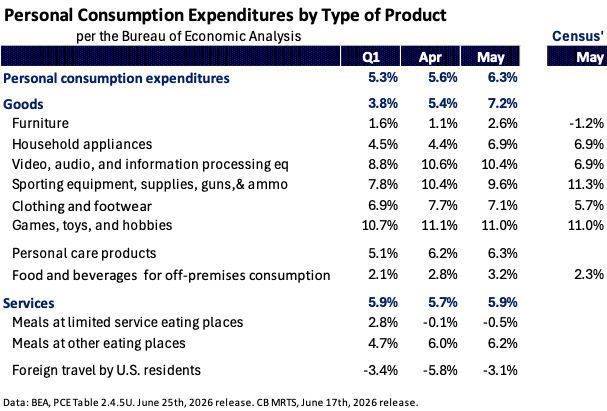

This is a follow-up note to help explain why nominal consumer spending and core* retail sales ran stronger (May) than we (per our data) and others expected. As we mentioned in the last note, inflation has accelerated (from Q1) in several categories, including sporting goods, clothing, consumer electronics, and grocery, and that’s pushing the nominal numbers higher. The inflation in consumer electronics (+8.3%), stems from the higher cost of memory and other components vis-à-vis competition for data center componentry. Expenditure on household appliances is simply “very strong” and that isn’t inflation as the PCE price index for the category was -1.3% in May. (Its strength is a nice tailwind for Lowe’s and Home Depot). The only weaker category in May was meals at limited-service eating places (which we’ve covered here). Separately, the negative figure for foreign travel is a positive contributor to PCE, and it also means that discretionary spending that took place overseas last year is now contributing to consumer spending and retail sales in the US (thus, its contribution is 2X). Our conclusion, the US consumer continues to be “remarkable,” and contrary to our initial views, core retail sales remained firm in May. That’s favorable for overall economic growth and US retailers. Moreover, given the decline in gas prices, June should be a better month than we previously expected, and limited-service’s trend is improving, as shown in the following graph.