Last year, Vegas operators realized that they were losing too much business in the mass segment of the market and they amped up advertising dollars and packaged discounts to win back the love (international was also a problem, but that’s a more difficult solve.) Interestingly, Advan’s data and Vegas’ statistics show a much-improved trend for Q1, including during March (when the Iran conflict metastasized). As such, it appears that the gaming industry’s investment to spur a return to Vegas is showing early signs of success.

- Domestic arrivals to Harry Reid (LAS) were down only -3% in February, much improved from the prior -HSD trend. International deplanings are still down sharply (-10%). LAS hasn’t released its March numbers yet, but observed visits per Advan* shows further improvement for the month.

- The LVCAA tourism tracker reports a +2% increase in visitor volume for February, a +120bps improvement in hotel occupancy, a +3.6% improvement in drive in from California, and a +0.9% increase in Strip gaming revenue. The TTM figures for these were a respective, -6.5%, -340 bps, -1.7%, and -1.4%, thus, all improved.

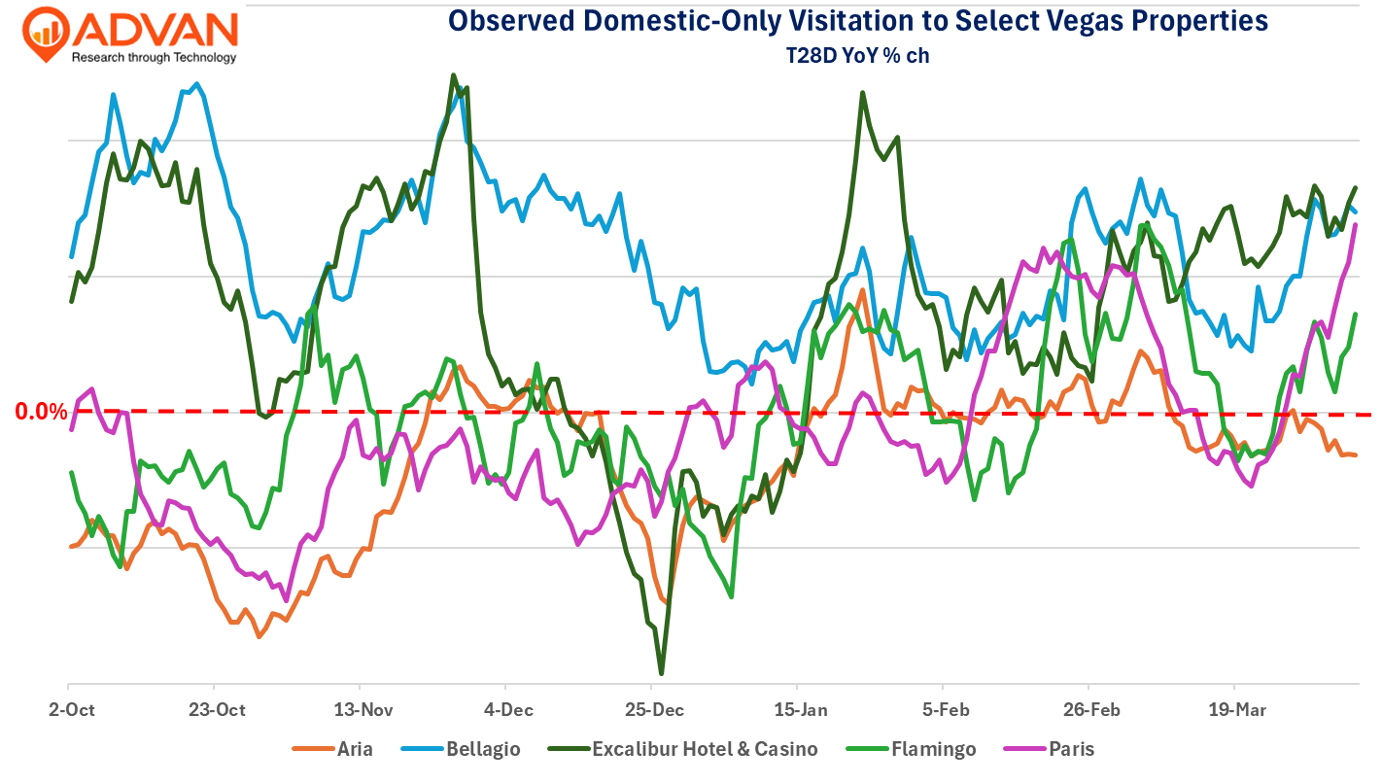

- For select casino resort properties, observed visits per Advan shows a marked improvement for mass from Q4’s trend. (The visits shown in the graph are only domestic visitors; the decline of international will pull the figures down.) RRR observed visits were a little softer (+3.0% vs. +5.5%), but the Red Rock Resort & Spa in Vegas had robust growth in visits and time on property**.

- For the high-end, like Bellagio / Venetian, the trend in observed visits (>30min) are largely consistent QoQ. Fontainebleau was stronger QoQ, whereas The Cosmopolitan and Wynn/Encore are softer QoQ. The Fontainebleau had a very strong Jan / Feb with time on property increasing +10%. For the high-end overall, we’d describe it as a wash QoQ. We suspect the Fontainebleau is impacting competitors (see Aria), and so it’s interesting that the Venetian, which sits between the Wynn and Cosmo / Aria, was consistent in Q1 (+4.5% in visits) with Q2 (+3.0%), with time spent up ahead of the +4.5% rate.

At a recent investor conference MGM CEO William Hornbuckle said, “We're excited by the trends we see in both of those parts of our business. We had nice Super Bowl. We had a great Chinese New Year's here. And so we feel good about that. I think we have second half of the year with the exception of leisure, which I'll speak to in a second. We have a soft second half of the year [2025). I think the general -- everybody did, us in particular. And so I think the opportunity to show growth ultimately in 2026 is very real and meaningful. And I think you'll see that from us is our expectation. We've got a lot of programming coming in, in April and May, throughout the summer, both short- and long-term programming that we think is going to be exciting for the destination. Leisure is a little different, although we've seen some green shoots slightly. It's too early to tell if it shifted back to where it was. Obviously, we own Excalibur and Luxor at the value and the chain. And we continue to see softness there. We are aggressively going out trying to do something about it through programming. You'll see us announce something in a couple of weeks, we think will be meaningful in that respect. And so we're excited for that to see where it goes. I think the market got caught flat-footed last summer because things were fine, and then in May suddenly they weren't. And so we're going to respond to that and respond to that aggressively.” Said differently, he likes the prospects of increased programming investments on top of an easy comparison base.

See our last write-ups on industry trends here and here.