- March retail sales growth (per the Census Bureau) was robust, fueled by the more affluent and the apparel / sportswear super-cycle (rapid GLP-1 adoption).

- Based on observed traffic (Advan) and earnings commentary from the credit card providers, April is lining up to again be a robust month, leading us to conclude that the US consumer is “just remarkable.“

- The strong Feb-Apr period sets up retailers well for earnings (in about four weeks). Brands that are much improved for the period include Target, Ulta, and Warby Parker.

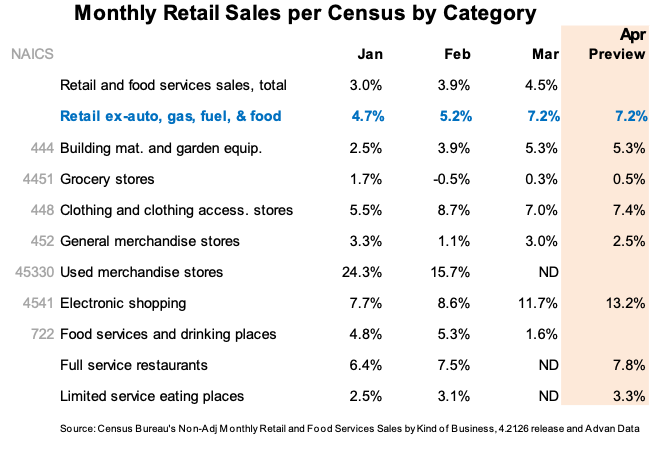

As previewed, March retail sales, per the Census Bureau’s monthly report, were robust and above market expectations (and our preview). Our definition of discretionary retail sales is the total, less gas, fuel, auto, and food, and we show that in the blue font in the table below. In light of gas prices and the Middle East, that discretionary spend accelerated during March is remarkable. Census’ seasonally adjusted figures tell a similar story, as did the commentary from the managements of bank and credit card providers during this earnings season. Luxury brands also spoke of acceleration in US demand (potentially due to less travel to Europe.) The March report also demonstrated that the macro trend of GLP-1 adoption remains at play, with the GLP-1 uptake fueling the apparel super-cycle and cutting spend at limited-service restaurants. Retail revenue growth for grocery also remains anemic as significant market share continues to flow to club, mass, and Amazon. Given the strength in “electronic shopping,” we expect Amazon to report robust top-line results for its North America Retail segment. On a more micro-level, secondhand stores remain very dynamic (see SVV). On a separate note, we’ve seen sell-side notes pointing to an abrupt slowdown in traffic during March at limited-service and off-price. As discussed in our preview, we see NO EVIDENCE of any traffic slowdown. (MCD should report solid traffic results).

April is a difficult month to analyze given the pull-forward of Easter to the 5th from last year’s 20th. We’ve made an attempt* to smooth things out, and based on our traffic data (and earnings results commentary), we believe that April will again be another strong month and in-line MoM, which will set up retailers favorably for their fiscal Q1 results. Brands that are much improved for the fiscal period include Target, Ulta, and Warby Parker. Let us know if you would like to delve into what we are observing.

On consumer spend and the affluent consumer, American Express CEO Stephen Squeri said, “We just had the strongest quarter of spending that we had in the last three years.” And on the risk of white-collar job cuts from AI (the latest bear thesis on the stock), Squeri said, “We're not seeing any impact at all on this at all. And maybe I'll just make a couple of comments. I think technological change over the years, no matter what it has been, whether it's been the Internet, the cell phone, what have you and even eliminating the word processor and going to desktop PCs has always brought a plethora of new jobs, number one; and number two, has fueled GDP. Now will AI lose some jobs? Yes, it would. But who would have thought about influencers, podcasters, web developers, AI programmers years ago. Probably nobody. And if you think about the jobs that are out there today, and where these jobs are, again, I think more your Gen Zs and Millennials are going to be more trained for this and more ready for this.”“

And so will jobs go away? Yes, jobs will go away. A number of the service jobs will go away. I mean, even at American Express today, if you look at our volume increase and you look at our ratio of volume to how many people we have on the phones, it's decreased. Not as many people want to talk on the phones and plus we're making the people that are answering the phones more efficient because they have AI tools at their disposal, whether that's for travel or whether that's for card servicing. We'll always have a representative there that you can call up and talk to, that's never going to go away from American Express. We're always going to be able to serve our customers how they want to be served. But I think from an AI perspective, yes, you'll see a bunch of jobs go away, but I think you'll also see a tremendous creation of new jobs. And I think this cohort will be much more likely to fill those jobs and create new jobs, new opportunities. The last thing I'll say is a lot of people talk about white collared workers. Our base is not just white-collared workers… So I think that will be there, and we'll see how it all plays out. But again, technology has, over time, fueled GDP, not crushed GDP.”*”Attempt” implies a larger degree of uncertainty to our figures and POV.