Key points:

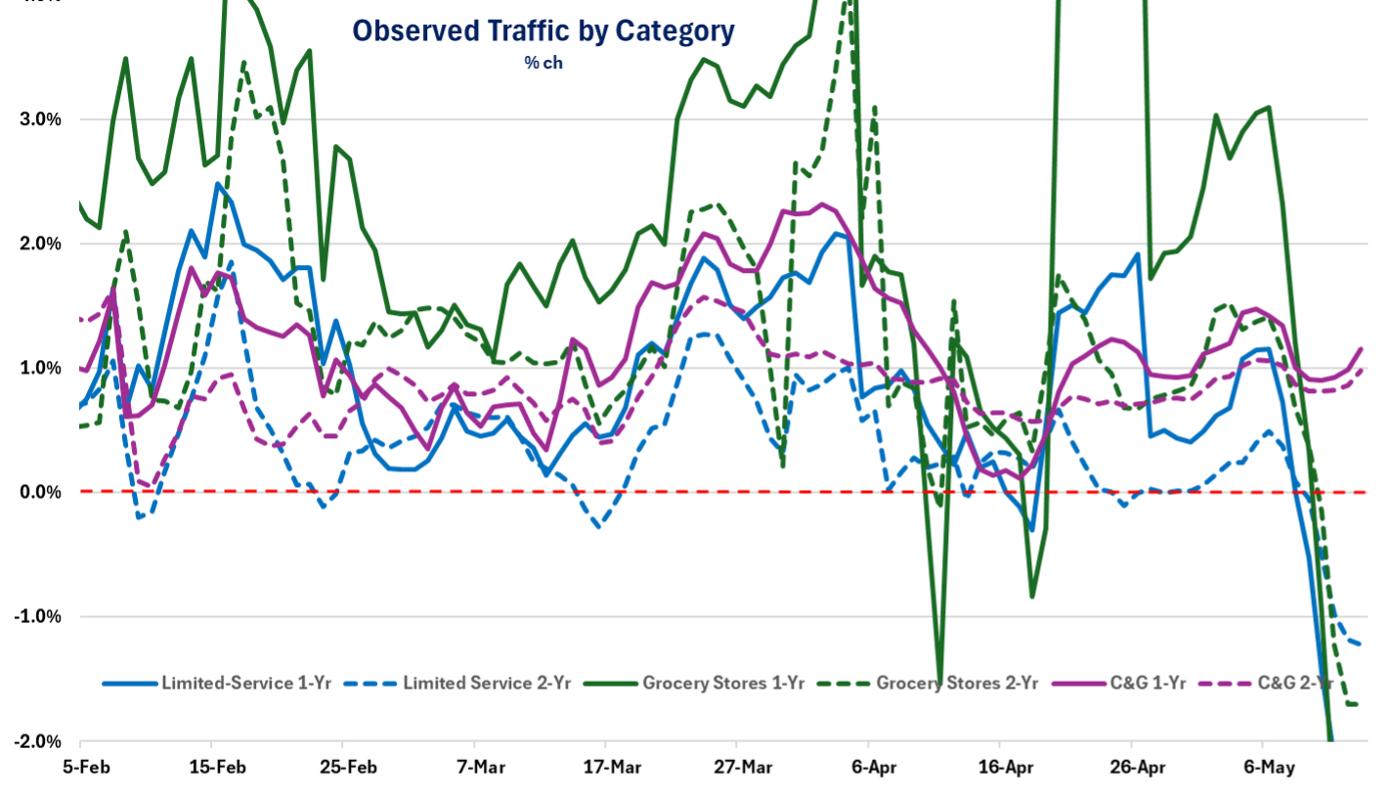

- April retail sales were strong, as previewed; however, May’s observed traffic (per Advan) is showing pockets of weakness in limited-service restaurants and conventional grocers.

- This was somewhat inevitable given the jump in gas prices, with high prices lasting longer than initially expected (or hoped for) and households now adjusting to a higher-for-longer scenario.

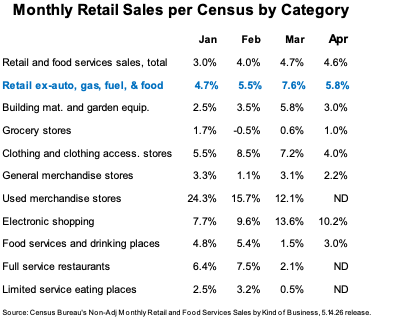

April retail sales (as reported by the Census Bureau) were strong, as previewed, but slightly below our estimates. However, March was upwardly revised and we expect that same will happen to the April numbers when the revisions are released in next month’s release. The biggest negative surprise in April was the slowdown in clothing and clothing accessories stores (recall our theme that the apparel category is experiencing a super-cycle fueled by the rapid update in GLP-1 drugs). As such, we will be carefully reviewing the April PCE report on May 28th. April was a stronger month for grocery and food services & drinking places; that’s primarily due to better weather.

Looking forward, May’s observed traffic (per Advan) for grocery stores and limited-service restaurants has softened. By contrast, convenience & gas, dollar stores, McDonald’s*, and Walmart (proxies for consumer spending) have remained resilient. The softness may be due to some consumers feeling fatigued from the high prices at the pump; that was inevitable. Earlier, less-affluent households could accept the high prices because they believed it was only temporary, but now that we are 10 weeks in, the burden has become more lasting, and as a result, households are making adjustments. This past week, General Mills and Kraft-Heinz noted that trends have softened. That was also shown in the latest week in scanner data.