Key points:

- Ross Inc reported exceptional top- and bottom-line FQ1 results (and right in line with Advan’s observations) with comp-sales increasing +17% (the strongest on record) and earnings up +37%.

- An improved better-and-best selection, more shelves stocked-up, improved service levels / store conditions, and a contemporized and increased advertising campaign all contributed, as did a higher level of confidence across the organization. The stores were loaded with compelling treasure hunt finds, and Ross’ merchants are getting the first look at better supply and jumping on it. (In-store inventory was up around +20%.)

- As previewed, there was not slowdown in off-price retail during March; however, as we saw with Walmart and Target, observed traffic and sales have slowed recently, likely due to being on the backside of tax refunds and higher-for-longer gas prices.

- Ross’ Q2 guide (comps +6-7%) and Advan’s benchmarking of Ross shows that the brand has more upside.

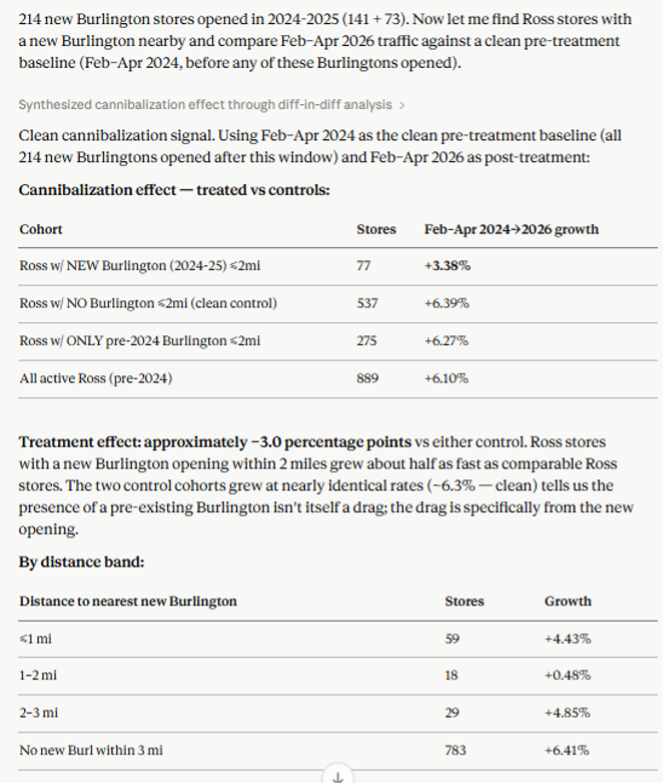

- Advan+Claude observations show an encroachment impact from new Burlington locations, with impacted stores growing traffic at half the rate of non-encroached stores.

- Should you want to talk about any of this, send me an e-mail.

Ross Stores, Inc reported a +17% comp-sales increase (inclusive of DDs), which was principally driven by comp-transactions. Advan observed traffic (per location) increased +5%, while improved conversion rate boosted observed traffic (+11%), and observed average ticket (+6%) increased due to Ross new elevated merchandise / brands offerings. New stores added 4 ppts to revenue growth, for a NSP figure of 100%. The traffic increase was principally driven by more customers (+5.4% per Advan), which stemmed from a more effective marketing campaign, as was the case in the 2H’25, i.e. Ross is getting better at it. The conversion rate improved due to a more attractive assortment (success by the merchants) and better in-stocks (stronger sourcing), and that’s also reflected in the increase in observed dwell-time (more surprise & delight in the stores). The strong NSP reflects success in new markets (Michigan and New Jersey) as well as densification in large existing markets (Texas and California).

CEO James Conroy said, “Our merchants and planners delivered compelling assortments and worked tirelessly to secure product to feed the outsized demand. Our supply chain network stepped up their efforts to keep the stores in stock in a timely manner. And finally, our stores team executed extremely well in supporting the increased product flow and customer activity… Performance at Ross was broad-based across both merchandise areas and geographies. While ladies and cosmetics were our strongest businesses, every major merchandise category posted comp growth in the teens or higher. Similarly, we saw strength across the entire country with the Midwest performing the best… We saw healthy increases in customer count on a comp store basis across income levels, ethnicities and all age groups, including the young customer.” Advan’s customer segmentation data supports Conroy’s statement, with Advan observed visits by psychographic segments up strongly for younger consumers as shown in the table below (we are using just California to keep the analysis on an apples-to-apples basis.)

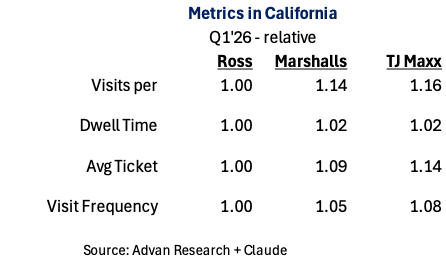

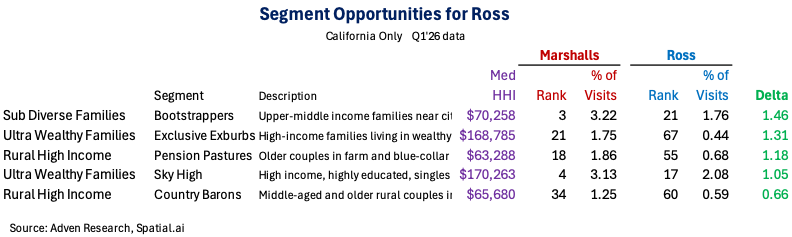

For most investors in ROST, the question is: how sustainable are the gains? Conroy said, “The company performed extremely well for years before I got here. I think if we made any changes, it's really a shift towards more focus on customer acquisition… So the health of our comp has been driven by transactions for the third consecutive quarter, and it's even more driven by transactions this quarter than even in the fourth quarter and the third quarter in terms of the transactions as a component of the overall comp. In terms of the durability, those transactions are driven by more customers… We're seeing that very strong growth across all ethnicities, all age groups, including the young customer, all income levels. And then if you think about the flywheel concept of bringing in more customers through marketing initiatives, great in-store environment, great merchandise selection, getting them in the store, converting shoppers into buyers with just compelling assortments and tidier stores and better in-store merchandising… The merchants are constantly opening up new brands. We found the confidence now to introduce brands that are more in the better and best price points and add those to the great stable brands that we already have. So that may give us some more comp increase the stores have proven that they can contribute to the store growth, but they are in the very early stages of changing visual merchandising and store labor models and shifting hours, reallocating store labor hours to sales driving activities… And that just drives more comp store sales. It gives you more store labor and more marketing, and we talked about this on the last call…. We're really trying to modernize the creative message. We're mixing up our media mix. We're doing more events. All of those things are adding to the proverbial top of funnel… I think that we're in the very, very early stages of focusing on the Ross and dd's brands contemporizing them and having them get their own sort of followership. And you can see it, right? You can follow us on social media. You can see our television spots. And it's -- I think it's a very refreshed view of how to go to market in retailing and certainly in off-price retailing.... We just have gotten started on many of these initiatives. So, I think it is durable.”The way an financial analyst would typically look at the potential is to compare Ross’s sales productivity to TJX’s, but, because of geographic differences, Ross at $508/sq-ft already exceeds Marmaxx, $479/sq-ft (2025 figures). However, Advan observed shows (using just California to keep the analysis on an apples-to-apples basis) that Ross has opportunity on all the principal KPIs: visits, visit frequency, dwell time, and average ticket. Consumer segment-wise, Ross has opportunity with two very affluent segments, Exclusives Exburbs (#21 out of 80 for Marshalls vs. #67 for Ross) and Sky High (#4 vs. #17). Both of these segments saw a decline in their % of visits for Ross in Q1, but we suspect that given Ross’ brand elevation strategy and new marketing, that focusing on customer recruitment of more affluent segments is a large opportunity for the brand. On availability of better and best brands, Conroy, “The other great thing is I think the market is now recognizing that our growth rate is a bit outsized. And we're getting a lot of first calls now.”

Separately, Burlington is opening a lot of new stores in Ross near-markets (77 out of 214 new stores over the past two years). We’ve cut and pasted the Advan+Claude analysis next. It appears that a new Burlington store will dimmish traffic to a nearby Ross store by about -300bps. Better customer segmentation, a more localized-merchandise assortment, and a better targeted local advertising should allow Ross to cut that level of encroachment, and drive stronger overall comp-sales.