Key points:

- As previewed, Apple delivered outstanding revenue results, driven by the iPhone and the US, along with Verizon delivering stronger postpaid phone net adds (previewed). By contrast, T-Mobile’s was stronger than we previewed, namely (in our view) because Charter fell short.

- Switching activity was higher YoY, which is what observed traffic implied, but overall activity was also higher as the industry produced another strong +4.6% growth in postpaid phone lines vs. only +0.6% population growth.

- Charter is being impacted by: satellite in rural areas, fiber overbuilds, FWA expansion, and its unwillingness to match the Big-3’s iPhone promotions.

- From the commentary, the operators want to de-escalate the handset promotions and move to wireless + broadband bundled packages which they believe offer greater LTV.

- Should you want to talk about any of this, send me an e-mail. (Find our Amazon preview here.)

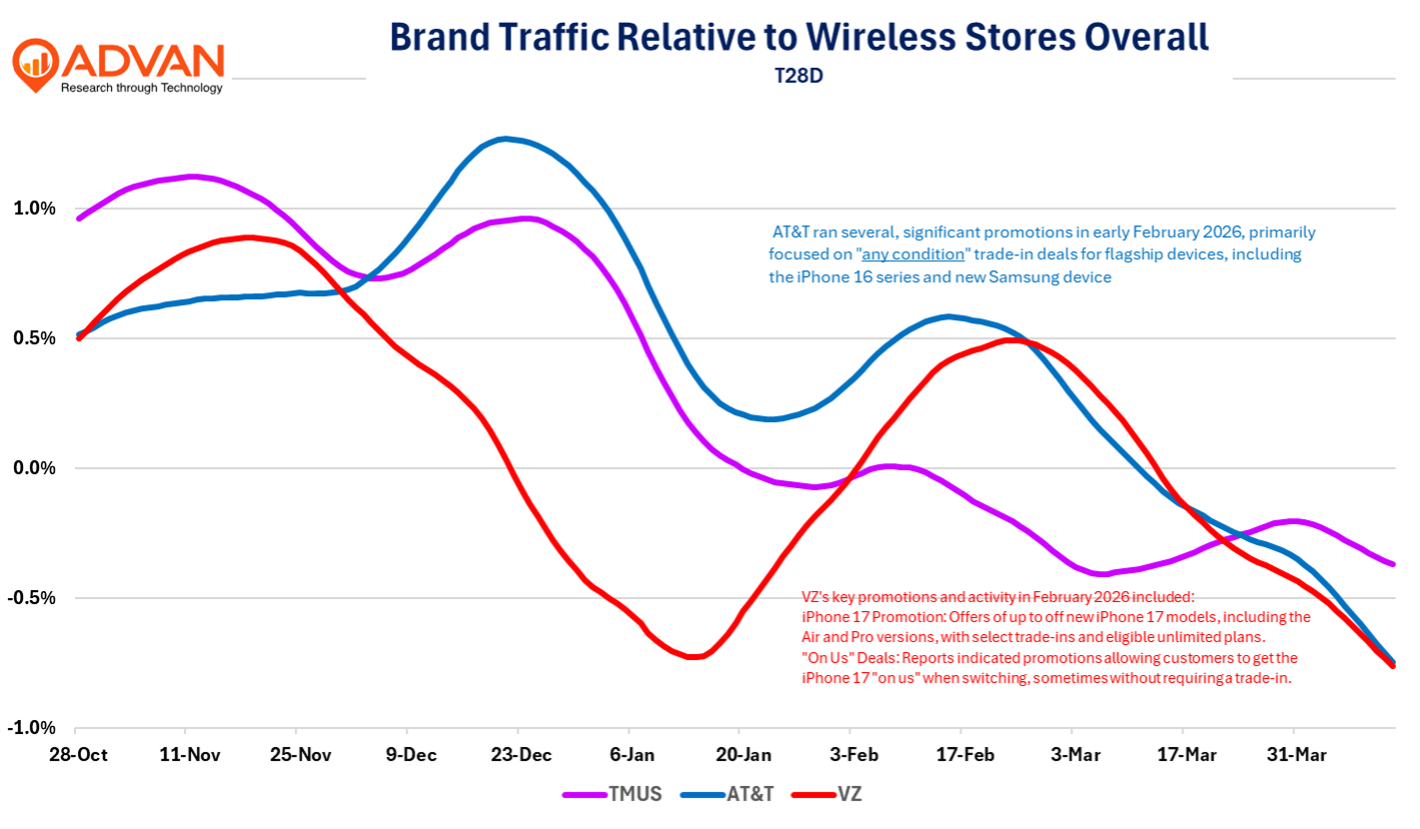

This note reviews the trends in telecom for the 1st quarter reporting period and the iPhone, all within the context of our preview and Q4’s, which was a blow-out for the iPhone and which also was a quarter of a lot of switching activity. We expected more of the same, but for cable’s share of net postpaid phone (the metric that’s of focus for this piece) adds to step up meaningfully. It did (47.9% from LQ’s 28.4%), but less than what was expected (50.3%) as Charter didn’t deliver. Additionally, T-Mobile did far better (524K*) than we expected (350K*). AT&T matched consensus expectations; Verizon outperformed (+55K vs. -83K). Verizon’s outperformance is the result of it resetting service plans at a greater value and its iPhone 17 promo, which produced a large lift during February.

As it relates to Apple, it reported blow-out top-line results, including the Americas segment revenue increasing +12% and iPhone revenue increasing +22%; on a 2-year organic CAGR basis, Americas accelerated 500bps QoQ and iPhone accelerated +170bps QoQ. While we all knew it, CEO Tim Cook shared, “ During the quarter, we welcomed iPhone 17E, the newest addition to what is already the strongest iPhone lineup we've ever had. It brings outstanding performance and core iPhone experiences at a remarkable value for everyone from enterprise teams to consumers. Across the lineup, this is the most powerful, capable and versatile iPhone family we've ever created.” As implied by the chart below, interest in Apple’s produces have remained high during April, providing supporting evidence for Apple’s strong CQ2 revenue guidance.

Our preview noted that we expected switching during the quarter to be high given the stronger observed traffic at wireless stores; however, while disconnects were more YoY, the rate of growth in disconnects slowed from previous quarters. We suspect that the bundling (fixed broadband + wireless) is changing the industry’s underlying customer dynamics. This hypothesis is supported by the fact that industry lines are accelerating despite population and household growth slowing; the Census Bureau puts 2026 growth at a modest +0.6%, meaningfully less than the industry’s +4.6%. (Census estimates that household growth is +1.25%.)

As it relates to bundling and new packaging, AT&T’s CEO John Stankey said, “You saw us lean into this advantage with the launch of AT&T OneConnect, the industry's first-ever single subscription service for fiber and wireless with a flat monthly price. This is how you should expect us to go to market as we accelerate the expansion of our fiber availability with offers and marketing strategies that yield attractive returns by driving deeper fiber penetration and growth in converged customer relationships. Running these plays has not only strengthened our performance in the consumer market, but they've begun to demonstrate that the same strategy can strengthen our business enterprise operations. During the first quarter, Advanced Connectivity business service revenue stabilized on a year-over-year basis for the first time ever…. The best things we have to drive customer retention and customer lifetime value is by pairing fiber broadband with wireless... It also tailors well into those account sizes that maybe are less than family plan sizes today that can grow over time.”

On convergence and offering greater value, Comcast CEO Mike Cavanaug, “Our [new promotion of offering a] free mobile line offer [to bundled customers] continues to perform well and is doing exactly what we intended, building awareness, increasing attachment, and expanding the top of the funnel across our broadband base.” And CFO Jason Armstrong said, “ A key metric for success is increasingly shifting toward consumer purchase intentions around bundled broadband and wireless offerings.” The near-term outcome of offering greater value was a -3.1% decline in broadband ARPU (the first decline on record) and -3.6% decline in mobile ARPU.

As it relates to T-Mobile’s outperformance, we suspect part of that is due to strong activity and wins in areas that that Advan doesn’t observe, like the business segment. CEO Srini Gopalan said, “In addition to our tremendous momentum in consumer across network seekers and other underpenetrated cohorts, our low share in T-Mobile for business also continues to give us substantial growth runway. This quarter, we continued to capture share with our network superiority-led value proposition in T-Mobile for Business.” Srini also said, “That's what's led us once again to grow our share of postpaid households in each of our cohorts in the top 100 cities.” (Advan doesn’t see many of the stores in large metro markets because they are on the ground level of a multi-story building; this is more acute because T-Mobile has a larger market share (40%) in the top-100 metros than its peers.)Srini and competitive actions / promotions in the quarter, “I'd say January was particularly competitive and particularly heavy in one-dimensional competition based on subsidies. I think Feb and March and going into April, we've seen some cooling down of that environment.“ A statement that describes the pattern we observed, as shown in the first chart above.

Lastly on Charter’s shortfall, CEO Chris Winfrey said, “We now have over 12 million mobile lines, including an increase of 370,000 Spectrum Mobile lines in the quarter. That's 1.8 million new lines over the last 12 months for growth over 17%. We're pleased with that growth given the continued intensity of mobile subsidies from the three big telcos. In internet, competition for new customers remains high, and our first quarter internet customer loss totaled 120,000.… Cable industry internet growth has been pressured for several years now, given new competition, a challenging housing environment and other factors like mobile substitution.” And CFO Jessica Fisher said, “We continue to see expanded fixed wireless competition and higher mobile substitution as well as ongoing fiber overlap growth at a rate similar to prior quarters. So I would point out that we also continue to have higher market share than our competitors, even in mature fiber markets. Collectively, that drove first quarter internet sales lower year-over-year. Churn improved year-over-year, and internet churn, including non-pay churn, remains at very low levels. In mobile… Net adds in the quarter were lower due to heavy device subsidy activity by the big three telco competitors, including the iPhone 17.“